What Our Clients Are Saying

Questions Answered: Buying airline stock? How long do bear markets last? Rebalancing?

Posted on:

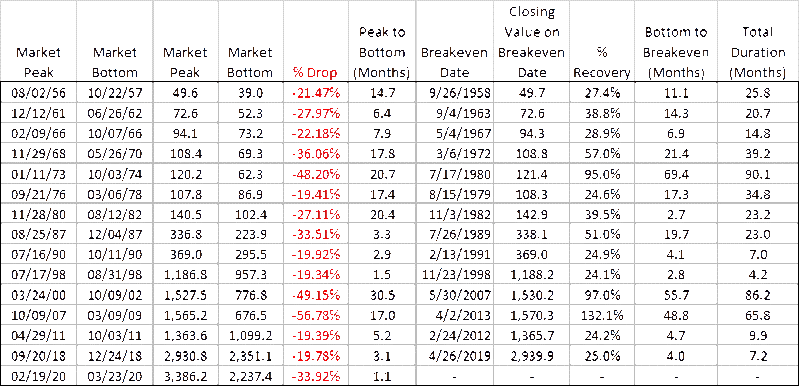

May 26, 2020Q1: How long does it usually take fully recover from a bear market?

Since 1950, the S&P 500 Index has gone through 15 bear markets by my count (including the current bear market):

*Market bottom, bear market duration, and total drop for 2020 bear market are as of 4/21/2020 and may get worse in the future. *All data comes from YCharts *Past performance is no guarantee of future results

The average length of those complete bear market cycles (peak to trough and back to breakeven) has averaged 32 months – just 2.5 years from the beginning of the downturn.

Q2: We are looking at a lot of industries that were particularly hit by this bear market (i.e. airlines, cruises, etc), is it wise to invest in these industries in economic downturns?

When we rebalance a properly diversified portfolio in the midst of a bear market it will automatically buy more of whatever sectors and companies have been hit the hardest while selling a bit of whatever has done best. In this way, rebalancing does actually put more emphasis on those parts of the market that have been hit hardest during a bear market. I would strongly caution against buying a individual stocks or sectors outside of a disciplined rebalancing strategy in the context of a thoroughly diversified portfolio though. Ultimately, these types of efforts fall into the two primary traps we see: security selection and market timing. Let’s take an example to show you what I mean.

Today, we’re in the middle of a bear market caused primarily by the coronavirus pandemic. This bear market has hit the travel industry particularly hard since far fewer people are interested in traveling. So, airlines and cruise ship companies have really suffered. In moments like this it can be tempting to want to buy airline stocks or cruise ship stocks because they appear to be selling at such a low price right now. While this instinct is better than allowing fear of the markets push you out of stocks altogether I believe it is still a mistake – more because of the mentality it fosters than the actual tactical decision to buy more of what’s down. In situations like this, most people are not talking about buying airline and cruise ship companies in the context of a thoroughly diversified portfolio. Rather, they are talking about taking cash or a part of their diversified portfolio and concentrating it in those types of companies. It is falling into the trap of believing that choosing the right investment (security selection) is the key to investment success. Ultimately, our behavior will trump any benefit we get out of buying the best investment right before it shoots up. So I don’t like the mindset of focusing on trying to identify the “best” investments. What we know is if we own a thoroughly diversified portfolio of stocks, it will include airline companies and cruise ship companies. Those types of companies would have been hit the hardest in this kind of downturn. So when we simply stick with our discipline of rebalancing our thoroughly diversified portfolio of stocks then we will automatically be buying more of those stocks than any others – simply because they’ve been hit the hardest. And we do it without slipping into the mindset that we can outsmart the markets or the economy and identify the “best” investment ahead of time.

Q3: What processes do you use in valuing a company and its stock prices to know if it’s a good long-term investment?

We generally do not recommend buying individual stocks and would much rather see our clients invest using mutual funds and exchange traded funds to build thoroughly diversified portfolios. But some of the ways we evaluate markets and companies are:

- The PE Ratio (Price-to-Earnings ratio): This is the price we have to pay today for each dollar of profits we expect from that company each year. A PE Ratio of 20 would mean that we would have to pay $20 today for every $1 of profits we’d expect from that company (or group of companies) each year going forward. And of course we would hope that $1 of profits would be more than $1 in future years. Companies self-report their income and expenses though and the primary purpose of that self-reporting is for tax purposes rather than investment analysis so there are distortions that can affect the analysis. One way we can address some of those issues is by looking at:

- The Price-to-Cash Flow analysis: This is the price we have to pay today for each dollar of “Free Cash Flow” we expect from that company each year. Free Cash Flow is, theoretically, money a business could use to pay out to owners some of the profits it has earned during the year. But there is no requirement that they pay out everything they have earned so we may want to analyze:

- The Dividend Yield: This is amount we would expect to receive in dividends from the business over the next year compared to the price we have to pay to buy the stock today. We might also want to analyze:

- The Price to Sales Ratio: This compares the price we pay today to the total amount of revenue a business receives from selling its products and services. Sales figures are much harder to manipulate and are generally considered more reliable than earnings.

Most fundamental stock analysis focuses on these issues and refinements of these different figures. For example, instead of taking a stock analysts word for it, it may be useful to forecast your own estimate of the earnings/profits you would expect the company to generate while you plan to own it.

Then you can bring those profits back to value in today’s dollars and more appropriately value the company for your investment time horizon so you can compare it’s value (based on your estimates) to the current market price to see if the market overvalues or undervalues the company compared to your analysis. Stock investment analysis can be extremely complicated and there is no end to the refinements that can be applied. Ultimately we want to buy good companies at good prices and hold on for the long term. An investment strategy that gets thoroughly diversified, rebalances when the portfolio drifts from its target mix, and holds on through the ugly times does exactly that.

Q4: Do you rebalance the portfolios you manage for your clients? How often?

In much of the investment industry, rebalancing is thought of as a calendar to-do item – it’s January 1st? Must be time to rebalance! Or they might rebalance quarterly or monthly, etc. At Tumwater we think rebalancing should happen only when things get out of balance. We believe it’s important that we monitor each investment in each client portfolio on a daily basis so we will know when it gets out of balance and will be able to take action to put things right again. At the same time, we don’t want to be trading client accounts when they’re just a fraction of a percentage point off of their targets. That would have us trading constantly and costing our clients a fortune in transaction costs. We’ve found a happy medium at roughly a 15-20% tolerance band for each investment. For example, imagine you have a fund into which you would like to invest 25% of your portfolio. A 20% tolerance band would mean you wouldn’t want that fund to ever be more than 30% of your portfolio (25% x 120% = 30%) or less than 20% of your portfolio (25% x 80% = 20%). If it ever drifted outside of that tolerance band it would be time to rebalance the portfolio to get it back to 25% of the portfolio. The beauty of a strict rebalancing discipline is that it institutionalizes the old investing formula: buy low, sell high. When a fund drops more than everything else in the portfolio it will drift below its lower tolerance band and we’ll be prompted to buy more of it – buy low. When a fund outperforms everything else in our portfolio it will drift above its higher tolerance band and we’ll be prompted to sell some of it – sell high. Repeated consistently over years and decades, the rebalancing discipline can enable investors to even outperform their own investments simply because they are buying more of the investment when it’s price is low and selling a bit of the investment when it’s price is high. That’s why we believe rebalancing to be a critical element to successful investment management over time.

Q5: I understand rebalancing on the way down (buying the dip) but why rebalance on the way up? Why not wait until the stock market has returned to a bull market? Wouldn’t this maximize gains during the market rise?

Ultimately, this question boils down to what is the right tolerance band for your rebalancing discipline. As the question implies, we don’t want to be selling stocks in the early stages of a recovery. So if we rebalance at the low point and the market begins to recover won’t that almost immediately prompt us to be selling some of the stocks we just bought? If we use a 15-20% tolerance band it’s important to realize that will prompt us to sell some of any particular fund only when it has gone up 15-20% more than all the other investments in the account rather than just whenever it happens to rise 15-20% in absolute terms.

For example, imagine if we had just 2 mutual funds in our portfolio, each with a target of 50%. If the total portfolio value is $100,000 then we’d want $50,000 in each investment. If both investments went up exactly 10% then nothing gets out of balance at all. The total portfolio would be $110,000, Fund 1 would be $55,000 and Fund 2 would be $55,000. Each investment would still be 50% of the overall portfolio. We only get drift from our targets when an investment performs differently than the rest of the portfolio. To take that example one step further, imagine the Fund 1 goes up 20% while Fund 2 goes up just 5%. Now Fund 1 is worth $60,000, Fund 2 is worth $52,500, and the total portfolio is worth $112,500. In that case, Fund 1 is now 53.3% of the portfolio while Fund 2 is 46.7% of the portfolio. Both are still well within their 15-20% tolerance bands.

If we build broad enough tolerance bands, then generally it takes fairly significant market moves to prompt us to rebalance which not only reduces transaction costs over time but also keeps us selling stocks in the early stages of a recovery while still maintaining a strict rebalancing discipline to avoid portfolios getting meaningfully more aggressive or more conservative by accident.

Disclosure:

Tumwater Wealth Management is a registered investment adviser and may only conduct business in states where it is registered or exempt. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.

Build a Retirement Income Plan that Gives You Confidence and Freedom

Sign up for our Retirement Income Planning Course.

Learn more